Training neural networks is often done by measuring many different metrics such as accuracy, loss, gradients, etc. This is most of the time done aggregating these metrics and plotting visualizations on TensorBoard.

There are, however, other senses that we can use to monitor the training of neural networks, such as sound. Sound is one of the perspectives that is currently very poorly explored in the training of neural networks. Human hearing can be very good a distinguishing very small perturbations in characteristics such as rhythm and pitch, even when these perturbations are very short in time or subtle.

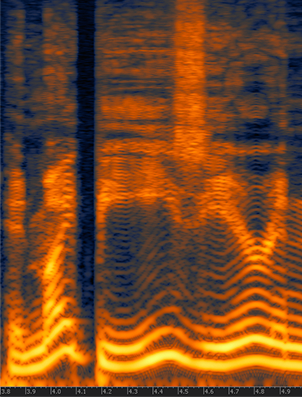

For this experiment, I made a very simple example showing a synthesized sound that was made using the gradient norm of each layer and for step of the training for a convolutional neural network training on MNIST using different settings such as different learning rates, optimizers, momentum, etc.

You’ll need to install PyAudio and PyTorch to run the code (in the end of this post).

Training sound with SGD using LR 0.01

This segment represents a training session with gradients from 4 layers during the first 200 steps of the first epoch and using a batch size of 10. The higher the pitch, the higher the norm for a layer, there is a short silence to indicate different batches. Note the gradient increasing during time.

Training sound with SGD using LR 0.1

Same as above, but with higher learning rate.

Training sound with SGD using LR 1.0

Same as above, but with high learning rate that makes the network to diverge, pay attention to the high pitch when the norms explode and then divergence.

Training sound with SGD using LR 1.0 and BS 256

Same setting but with a high learning rate of 1.0 and a batch size of 256. Note how the gradients explode and then there are NaNs causing the final sound.

Training sound with Adam using LR 0.01

This is using Adam in the same setting as the SGD.

Source code

For those who are interested, here is the entire source code I used to make the sound clips:

import pyaudio

import numpy as np

import wave

import torch

import torch.nn as nn

import torch.nn.functional as F

import torch.optim as optim

from torchvision import datasets, transforms

class Net(nn.Module):

def __init__(self):

super(Net, self).__init__()

self.conv1 = nn.Conv2d(1, 20, 5, 1)

self.conv2 = nn.Conv2d(20, 50, 5, 1)

self.fc1 = nn.Linear(4*4*50, 500)

self.fc2 = nn.Linear(500, 10)

self.ordered_layers = [self.conv1,

self.conv2,

self.fc1,

self.fc2]

def forward(self, x):

x = F.relu(self.conv1(x))

x = F.max_pool2d(x, 2, 2)

x = F.relu(self.conv2(x))

x = F.max_pool2d(x, 2, 2)

x = x.view(-1, 4*4*50)

x = F.relu(self.fc1(x))

x = self.fc2(x)

return F.log_softmax(x, dim=1)

def open_stream(fs):

p = pyaudio.PyAudio()

stream = p.open(format=pyaudio.paFloat32,

channels=1,

rate=fs,

output=True)

return p, stream

def generate_tone(fs, freq, duration):

npsin = np.sin(2 * np.pi * np.arange(fs*duration) * freq / fs)

samples = npsin.astype(np.float32)

return 0.1 * samples

def train(model, device, train_loader, optimizer, epoch):

model.train()

fs = 44100

duration = 0.01

f = 200.0

p, stream = open_stream(fs)

frames = []

for batch_idx, (data, target) in enumerate(train_loader):

data, target = data.to(device), target.to(device)

optimizer.zero_grad()

output = model(data)

loss = F.nll_loss(output, target)

loss.backward()

norms = []

for layer in model.ordered_layers:

norm_grad = layer.weight.grad.norm()

norms.append(norm_grad)

tone = f + ((norm_grad.numpy()) * 100.0)

tone = tone.astype(np.float32)

samples = generate_tone(fs, tone, duration)

frames.append(samples)

silence = np.zeros(samples.shape[0] * 2,

dtype=np.float32)

frames.append(silence)

optimizer.step()

# Just 200 steps per epoach

if batch_idx == 200:

break

wf = wave.open("sgd_lr_1_0_bs256.wav", 'wb')

wf.setnchannels(1)

wf.setsampwidth(p.get_sample_size(pyaudio.paFloat32))

wf.setframerate(fs)

wf.writeframes(b''.join(frames))

wf.close()

stream.stop_stream()

stream.close()

p.terminate()

def run_main():

device = torch.device("cpu")

train_loader = torch.utils.data.DataLoader(

datasets.MNIST('../data', train=True, download=True,

transform=transforms.Compose([

transforms.ToTensor(),

transforms.Normalize((0.1307,), (0.3081,))

])),

batch_size=256, shuffle=True)

model = Net().to(device)

optimizer = optim.SGD(model.parameters(), lr=0.01, momentum=0.5)

for epoch in range(1, 2):

train(model, device, train_loader, optimizer, epoch)

if __name__ == "__main__":

run_main()

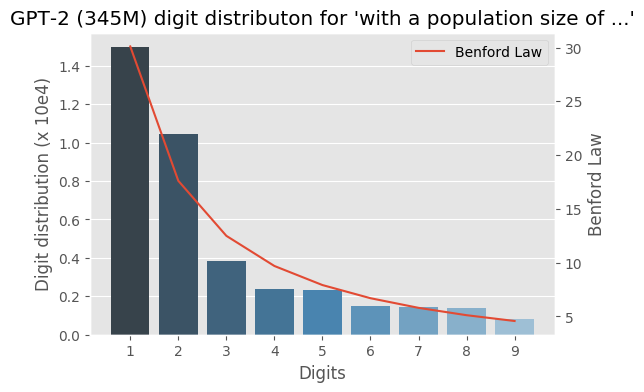

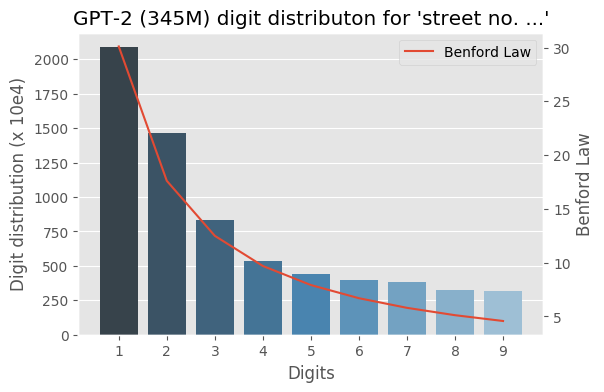

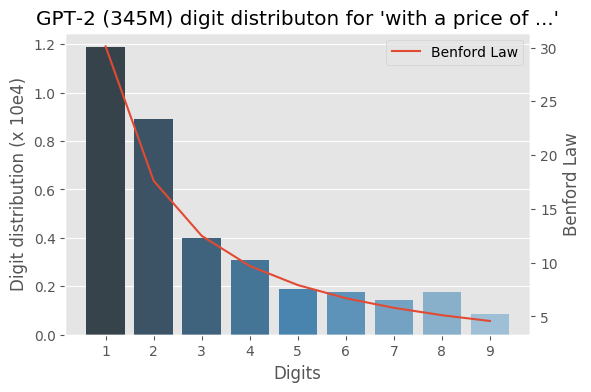

I wrote some months ago about how the Benford law emerges from language models, today I decided to evaluate the same method to check how the GPT-2 would behave with some sentences and it turns out that it seems that it is also capturing these power laws. You can find some plots with the examples below, the plots are showing the probability of the digit given a particular sentence such as “with a population size of”, showing the distribution of: $$P(\{1,2, \ldots, 9\} \vert \text{“with a population size of”})$$ for the GPT-2 medium model (345M):

Trained MLP with 2 hidden layers and a sine prior.

I was experimenting with the approach described in “Randomized Prior Functions for Deep Reinforcement Learning” by Ian Osband et al. at NPS 2018, where they devised a very simple and practical method for uncertainty using bootstrap and randomized priors and decided to share the PyTorch code.

I really like bootstrap approaches, and in my opinion, they are usually the easiest methods to implement and provide very good posterior approximation with deep connections to Bayesian approaches, without having to deal with variational inference. They actually show in the paper that in the linear case, the method provides a Bayes posterior.

The main idea of the method is to have bootstrap to provide a non-parametric data perturbation together with randomized priors, which are nothing more than just random initialized networks.

$$Q_{\theta_k}(x) = f_{\theta_k}(x) + p_k(x)$$

The final model \(Q_{\theta_k}(x)\) will be the k model of the ensemble that will fit the function \(f_{\theta_k}(x)\) with an untrained prior \(p_k(x)\).

Let’s go to the code. The first class is a simple MLP with 2 hidden layers and Glorot initialization :

class MLP(nn.Module):

def __init__(self):

super().__init__()

self.l1 = nn.Linear(1, 20)

self.l2 = nn.Linear(20, 20)

self.l3 = nn.Linear(20, 1)

nn.init.xavier_uniform_(self.l1.weight)

nn.init.xavier_uniform_(self.l2.weight)

nn.init.xavier_uniform_(self.l3.weight)

def forward(self, inputs):

x = self.l1(inputs)

x = nn.functional.selu(x)

x = self.l2(x)

x = nn.functional.selu(x)

x = self.l3(x)

return x

Then later we define a class that will take the model and the prior to produce the final model result:

And it’s basically that ! As you can see, it’s a very simple method, in the second part we just created a custom forward() to avoid computing/accumulating gradients for the prior network and them summing (after scaling) it with the model prediction.

To train it, you just have to use different bootstraps for each ensemble model, like in the code below:

def train_model(x_train, y_train, base_model, prior_model):

model = ModelWithPrior(base_model, prior_model, 1.0)

loss_fn = nn.MSELoss()

optimizer = torch.optim.Adam(model.parameters(), lr=0.05)

for epoch in range(100):

model.train()

preds = model(x_train)

loss = loss_fn(preds, y_train)

optimizer.zero_grad()

loss.backward()

optimizer.step()

return model

and using a sampler with replacement (bootstrap) as in:

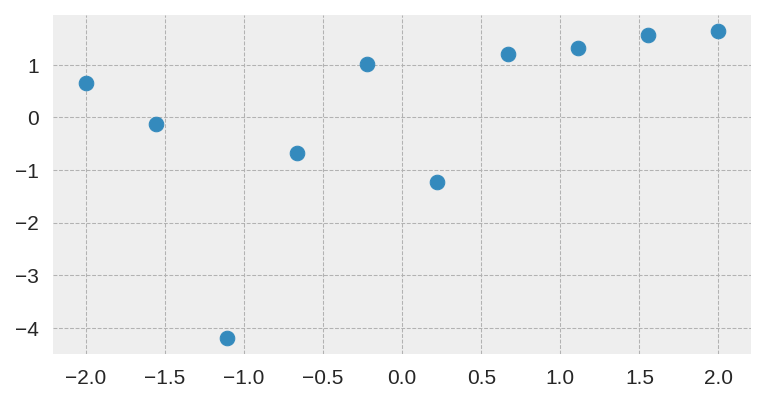

In this case, I used the same small dataset used in the original paper:

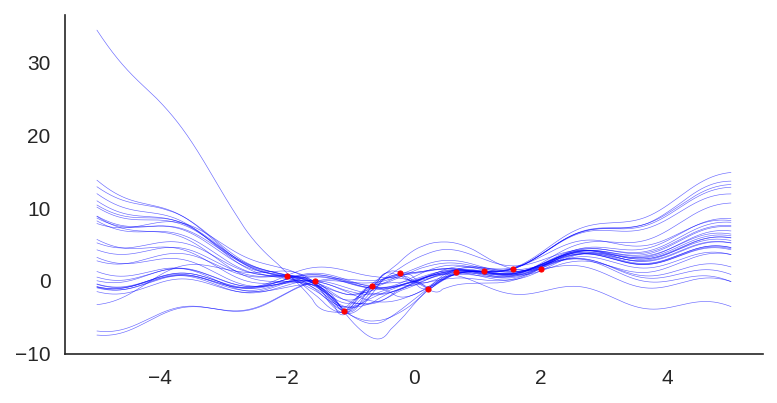

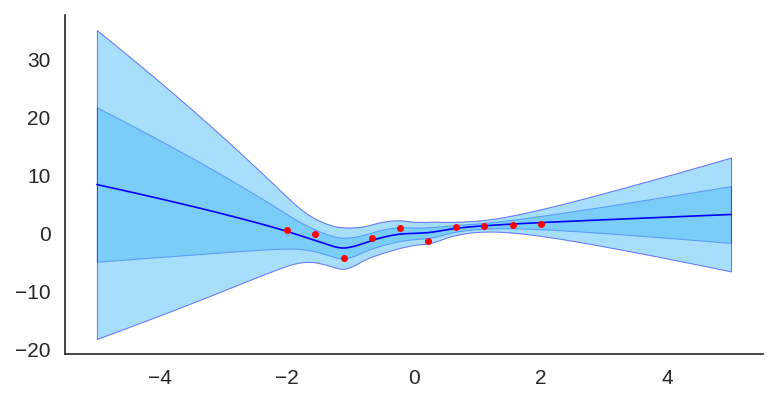

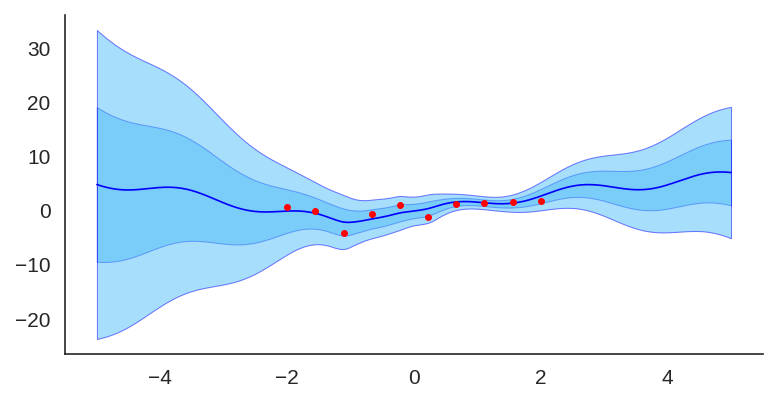

After training it with a simple MLP prior as well, the results for the uncertainty are shown below:

Trained model with an MLP prior, used an ensemble of 50 models.

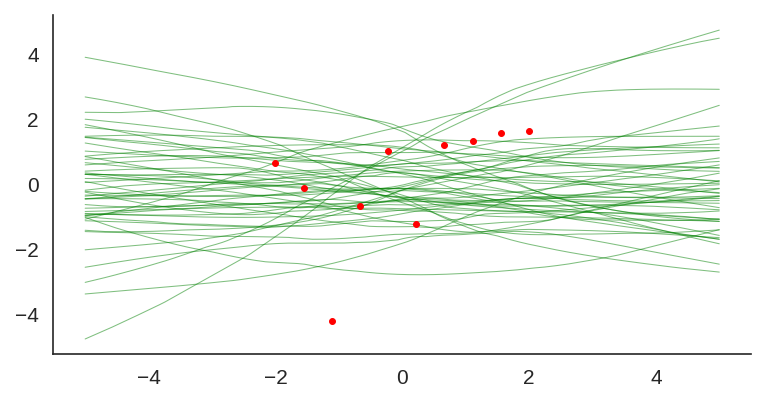

If we look at just the priors, we will see the variation of the untrained networks:

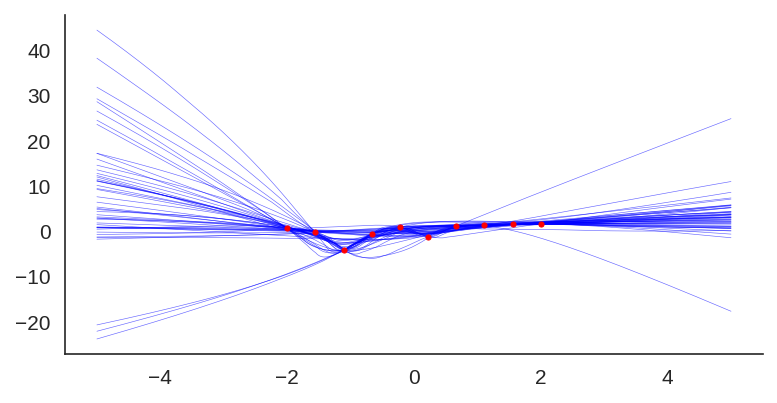

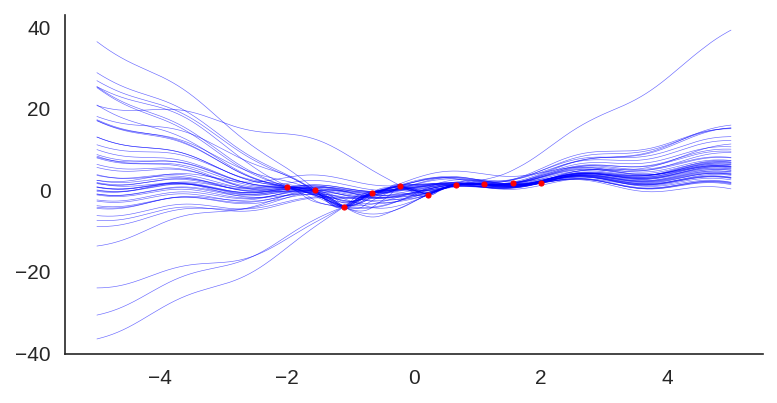

We can also visualize the individual model predictions showing their variability due to different initializations as well as the bootstrap noise:

Plot showing each individual model prediction and true data in red.

Now, what is also quite interesting, is that we can change the prior to let’s say a fixed sine:

class SinPrior(nn.Module):

def forward(self, input):

return torch.sin(3 * input)

Then, when we train the same MLP model but this time using the sine prior, we can see how it affects the final prediction and uncertainty bounds:

If we show each individual model, we can see the effect of the prior contribution to each individual model:

Plot showing each individual model of the ensemble trained with a sine prior.

I hope you liked, these are quite amazing results for a simple method that at least pass the linear “sanity check”. I’ll explore some pre-trained networks in place of the prior to see the different effects on predictions, it’s a very interesting way to add some simple priors.

It is frustrating to learn about principles such as maximum likelihood estimation (MLE), maximum a posteriori (MAP) and Bayesian inference in general. The main reason behind this difficulty, in my opinion, is that many tutorials assume previous knowledge, use implicit or inconsistent notation, or are even addressing a completely different concept, thus overloading these principles.

Those aforementioned issues make it very confusing for newcomers to understand these concepts, and I’m often confronted by people who were unfortunately misled by many tutorials. For that reason, I decided to write a sane introduction to these concepts and elaborate more on their relationships and hidden interactions while trying to explain every step of formulations. I hope to bring something new to help people understand these principles.

Maximum Likelihood Estimation

The maximum likelihood estimation is a method or principle used to estimate the parameter or parameters of a model given observation or observations. Maximum likelihood estimation is also abbreviated as MLE, and it is also known as the method of maximum likelihood. From this name, you probably already understood that this principle works by maximizing the likelihood, therefore, the key to understand the maximum likelihood estimation is to first understand what is a likelihood and why someone would want to maximize it in order to estimate model parameters.

Let’s start with the definition of the likelihood function for continuous case:

$$\mathcal{L}(\theta | x) = p_{\theta}(x)$$

The left term means “the likelihood of the parameters \(\theta\), given data \(x\)”. Now, what does that mean ? It means that in the continuous case, the likelihood of the model \(p_{\theta}(x)\) with the parametrization \(\theta\) and data \(x\) is the probability density function (pdf) of the model with that particular parametrization.

Although this is the most used likelihood representation, you should pay attention that the notation \(\mathcal{L}(\cdot | \cdot)\) in this case doesn’t mean the same as the conditional notation, so be careful with this overload, because it is always implicitly stated and it is also often a source of confusion. Another representation of the likelihood that is often used is \(\mathcal{L}(x; \theta)\), which is better in the sense that it makes it clear that it’s not a conditional, however, it makes it look like the likelihood is a function of the data and not of the parameters.

The model \(p_{\theta}(x)\) can be any distribution, and to make things concrete, let’s say that we are assuming that the data generating distribution is an univariate Gaussian distribution, which we define below:

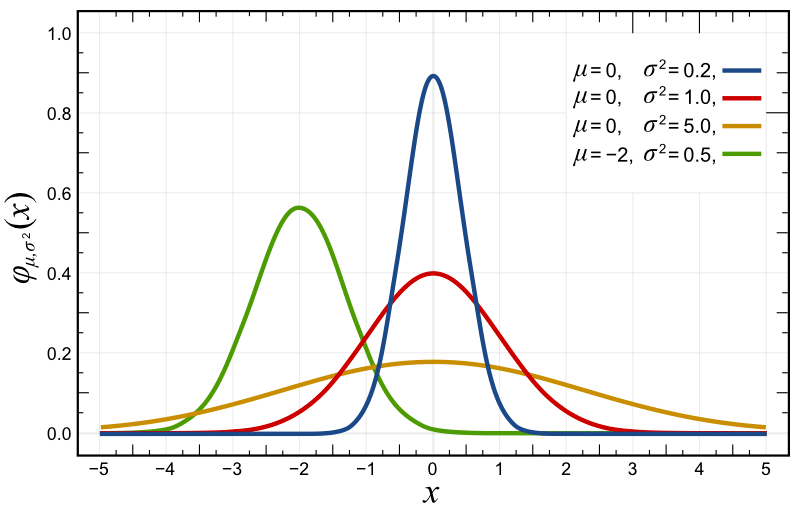

If you plot this probability density function with different parametrizations, you’ll get something like the plots below, where the red distribution is the standard Gaussian \(p(x) \sim \mathcal{N}(0, 1.0)\):

A selection of Normal Distribution Probability Density Functions (PDFs). Both the mean, μ, and variance, σ², are varied. The key is given on the graph. Source: Wikimedia Commons.

As you can see in the probability density function (pdf) plot above, the likelihood of \(x\) at variously given realizations are showed in the y-axis. Another source of confusion here is that usually, people take this as a probability, because they usually see these plots of normals and the likelihood is always below 1, however, the probability density function doesn’t give you probabilities but densities. The constraint on the pdf is that it must integrate to one:

$$\int_{-\infty}^{+\infty} f(x)dx = 1$$

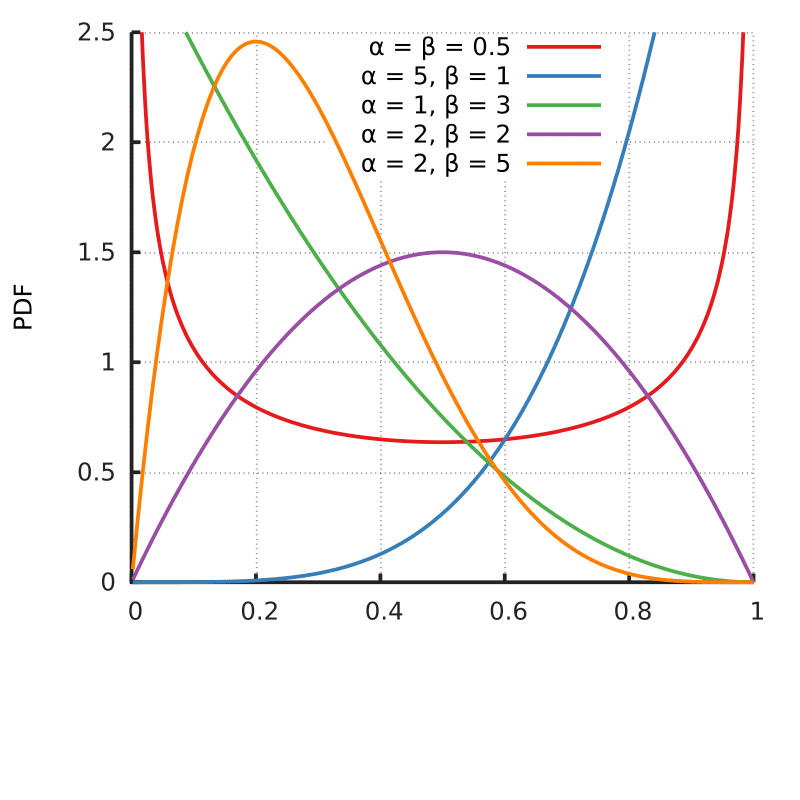

So, it is completely normal to have densities larger than 1 in many points for many different distributions. Take for example the pdf for the Beta distribution below:

Probability density function for the Beta distribution. Source: Wikimedia Commons.

As you can see, the pdf shows densities above one in many parametrizations of the distribution, while still integrating into 1 and following the second axiom of probability: the unit measure.

So, returning to our original principle of maximum likelihood estimation, what we want is to maximize the likelihood \(\mathcal{L}(\theta | x)\) for our observed data. What this means in practical terms is that we want to find the parameters \(\theta\) of our model where the likelihood that this model generated our data is maximized, we want to find which parameters of this model are most plausible to have generated this observed data, or what are the parameters that make this sample most probable ?

For the case of our univariate Gaussian model, what we want is to find the parameters \(\mu\) and \(\sigma^2\), which for convenient notation we collapse into a single parameter vector:

Because these are the statistics that completely define our univariate Gaussian model. So let’s formulate the problem of the maximum likelihood estimation:

This says that we want to obtain the maximum likelihood estimate \(\hat{\theta}\) that approximates \(p_{\theta}(x)\) to a underlying “true” distribution \(p_{\theta^*}(x)\) by maximizing the likelihood of the parameters \(\theta\) given data \(x\). You shouldn’t confuse a maximum likelihood estimate \(\hat{\theta}(x)\) which is a realization of the maximum likelihood estimator for the data \(x\), with the maximum likelihood estimator \(\hat{\theta}\), so pay attention to disambiguate it in your head.

However, we need to incorporate multiple observations in this formulation, and by adding multiple observations we end up with a complex joint distribution:

That needs to take into account the interactions between all observations. And here is where we make a strong assumption: we state that the observations are independent. Independent random variables mean that the following holds:

Which means that since \(x_1, x_2, \ldots, x_n\) don’t contain information about each other, we can write the joint probability as a product of their marginals.

Another assumption that is made, is that these random variables are identically distributed, which means that they came from the same generating distribution, which allows us to model it with the same distribution parametrization.

Given these two assumptions, which are also known as IID (independently and identically distributed), we can formulate our maximum likelihood estimation problem as:

Note that MLE doesn’t require you to make these assumptions, however, many problems will appear if you don’t to it, such as different distributions for each sample or having to deal with joint probabilities.

Given that in many cases these densities that we multiply can be very small, multiplying one by the other in the product that we have above we can end up with very small values. Here is where the logarithm function makes its way to the likelihood. The log function is a strictly monotonically increasing function, that preserves the location of the extrema and has a very nice property:

$$\log ab = \log a + \log b $$

Where the logarithm of a product is the sum of the logarithms, which is very convenient for us, so we’ll apply the logarithm to the likelihood to maximize what is called the log-likelihood:

As you can see, we went from a product to a summation, which is much more convenient. Another reason for the application of the logarithm is that we often take the derivative and solve it for the parameters, therefore is much easier to work with a summation than a multiplication.

We can also conveniently average the log-likelihood (given that we’re just including a multiplication by a constant):

This is also convenient because it will take out the dependency on the number of observations. We also know, that through the law of large numbers, the following holds as \(n\to\infty\):

As you can see, we’re approximating the expectation with the empirical expectation defined by our dataset \(\{x_i\}_{i=1}^{n}\). This is an important point and it is usually implictly assumed.

The weak law of large numbers can be bounded using a Chebyshev bound, and if you are interested in concentration inequalities, I’ve made an article about them here where I discuss the Chebyshev bound.

To finish our formulation, given that we usually minimize objectives, we can formulate the same maximum likelihood estimation as the minimization of the negative of the log-likelihood:

Which is exactly the same thing with just the negation turn the maximization problem into a minimization problem.

The relation of maximum likelihood estimation with the Kullback–Leibler divergence from information theory

It is well-known that maximizing the likelihood is the same as minimizing the Kullback-Leibler divergence, also known as the KL divergence. Which is very interesting because it links a measure from information theory with the maximum likelihood principle.

There are many intuitions to understand the KL divergence, I personally like the perspective on the likelihood ratios, however, there are plenty of materials about it that you can easily find and it’s out of the scope of this introduction.

The KL divergence is basically the expectation of the log-likelihood ratio under the \(p(x)\) distribution. What we’re doing below is just rephrasing it by using some identities and properties of the expectation:

In the formulation above, we’re first using the fact that the logarithm of a quotient is equal to the difference of the logs of the numerator and denominator (equation \(\ref{eq:logquotient}\)). After that we use the linearization of the expectation(equation \(\ref{eq:linearization}\)), which tells us that \(\mathbb{E}\left[X + Y\right] = \mathbb{E}\left[X\right]+\mathbb{E}\left[Y\right]\). In the end, we are left with two terms, the first one in the left is the entropy and the one in the right you can recognize as the negative of the log-likelihood that we saw earlier.

If we want to minimize the KL divergence for the \(\theta\), we can ignore the first term, since it doesn’t depend of \(\theta\) in any way, and in the end we have exactly the same maximum likelihood formulation that we saw before:

A very common scenario in Machine Learning is supervised learning, where we have data points \(x_n\) and their labels \(y_n\) building up our dataset \( D = \{ (x_1, y_1), (x_2, y_2), \ldots, (x_n, y_n) \} \), where we’re interested in estimating the conditional probability of \(\textbf{y}\) given \(\textbf{x}\), or more precisely \( P_{\theta}(Y | X) \).

To extend the maximum likelihood principle to the conditional case, we just have to write it as:

In that case, you can see that we end up with a sum of squared errors that will have the same location of the optimum of the mean squared error (MSE). So you can see that minimizing the MSE is equivalent of maximizing the likelihood for a Gaussian model.

Remarks on the maximum likelihood

The maximum likelihood estimation has very interesting properties but it gives us only point estimates, and this means that we cannot reason on the distribution of these estimates. In contrast, Bayesian inference can give us a full distribution over parameters, and therefore will allow us to reason about the posterior distribution.

I’ll write more about Bayesian inference and sampling methods such as the ones from the Markov Chain Monte Carlo (MCMC) family, but I’ll leave this for another article, right now I’ll continue showing the relationship of the maximum likelihood estimator with the maximum a posteriori (MAP) estimator.

Maximum a posteriori

Although the maximum a posteriori, also known as MAP, also provides us with a point estimate, it is a Bayesian concept that incorporates a prior over the parameters. We’ll also see that the MAP has a strong connection with the regularized MLE estimation.

We know from the Bayes rule that we can get the posterior from the product of the likelihood and the prior, normalized by the evidence:

In the equation \(\ref{eq:proport}\), since we’re worried about optimization, we cancel the normalizing evidence \(p(x)\) and stay with a proportional posterior, which is very convenient because the marginalization of \(p(x)\) involves integration and is intractable for many cases.

In this formulation above, we just followed the same steps as described earlier for the maximum likelihood estimator, we assume independence and an identical distributional setting, followed later by the logarithm application to switch from a product to a summation. As you can see in the final formulation, this is equivalent as the maximum likelihood estimation multiplied by the prior term.

We can also easily recover the exact maximum likelihood estimator by using a uniform prior \(p(\theta) \sim \textbf{U}(\cdot, \cdot)\). This means that every possible value of \(\theta\) will be equally weighted, meaning that it’s just a constant multiplication:

And there you are, the MAP with a uniform prior is equivalent to MLE. It is also easy to show that a Gaussian prior can recover the L2 regularized MLE. Which is quite interesting, given that it can provide insights and a new perspective on the regularization terms that we usually use.

I hope you liked this article ! The next one will be about Bayesian inference with posterior sampling, where we’ll show how we can reason about the posterior distribution and not only on point estimates as seen in MAP and MLE.

– Christian S. Perone

Cite this article as: Christian S. Perone, "A sane introduction to maximum likelihood estimation (MLE) and maximum a posteriori (MAP)," in Terra Incognita, 02/01/2019, https://blog.christianperone.com/2019/01/mle/.

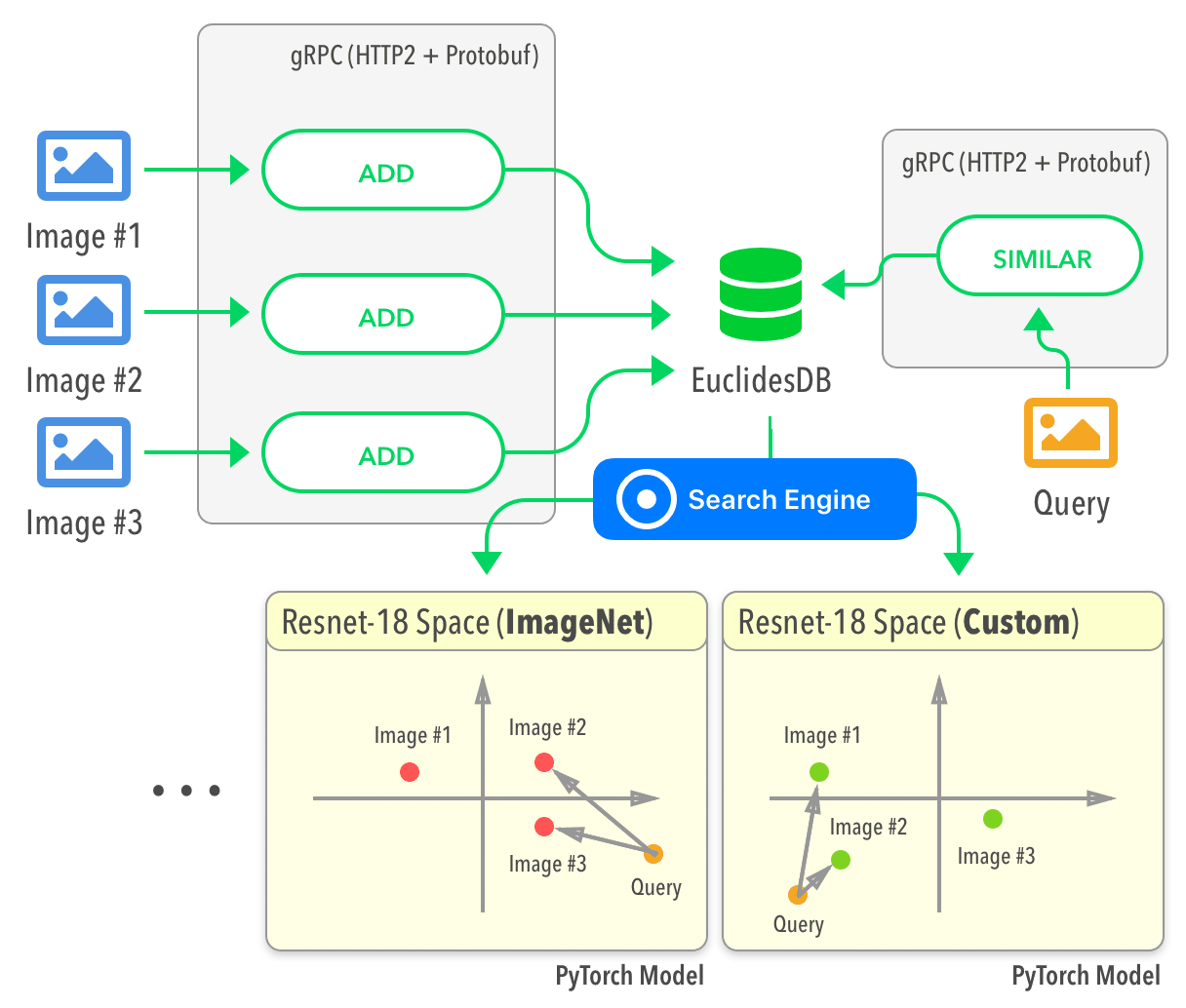

Past week I released the first public version of EuclidesDB. EuclidesDB is a multi-model machine learning feature database that is tightly coupled with PyTorch and provides a backend for including and querying data on the model feature space.

* This post is in Portuguese. It’s a bayesian analysis of a Brazilian national exam. The main focus of the analysis is to understand the underlying factors impacting the participants performance on ENEM.

Este tutorial apresenta uma análise breve dos microdados do ENEM do Rio Grande do Sul do ano de 2017. O principal objetivo é entender os fatores que impactam na performance dos participantes do ENEM dado fatores como renda familiar e tipo de escola. Neste tutorial são apresentados dois modelos: regressão linear e regressão linear hierárquica.

I was experimenting with the digits distribution from a pre-trained (weights from the OpenAI repository) Transformer language model (LM) and I found a very interesting correlation between the Benford’s law and the digit distribution of the language model after conditioning it with some particular phrases.

Below is the correlation between the Benford’s law and the language model with conditioning on the phrase (shown in the figure):

Today, at the PyTorch Developer Conference, the PyTorch team announced the plans and the release of the PyTorch 1.0 preview with many nice features such as a JIT for model graphs (with and without tracing) as well as the LibTorch, the PyTorch C++ API, one of the most important release announcement made today in my opinion.

Given the huge interest in understanding how this new API works, I decided to write this article showing an example of many opportunities that are now open after the release of the PyTorch C++ API. In this post, I’ll integrate PyTorch inference into native NodeJS using NodeJS C++ add-ons, just as an example of integration between different frameworks/languages that are now possible using the C++ API.

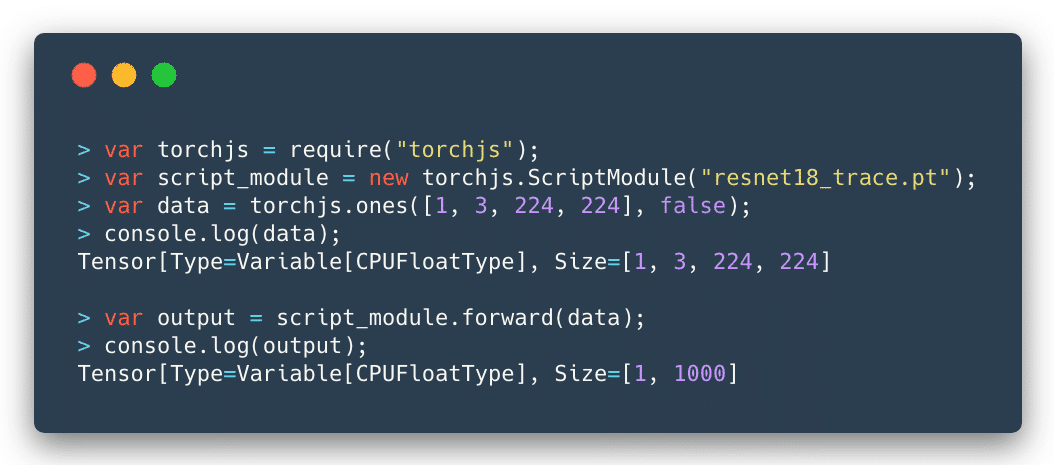

Below you can see the final result:

As you can see, the integration is seamless and I could use a traced ResNet as the computational graph model and feed any tensor to it to get the output predictions.

Introduction

Simply put, the libtorch is a library version of the PyTorch. It contains the underlying foundation that is used by PyTorch, such as the ATen (the tensor library), which contains all the tensor operations and methods. Libtorch also contains the autograd, which is the component that adds the automatic differentiation to the ATen tensors.

A word of caution for those who are starting now is to be careful with the use of the tensors that can be created both from ATen and autograd, do not mix them, the ATen will return the plain tensors (when you create them using the at namespace) while the autograd functions (from the torch namespace) will return Variable, by adding its automatic differentiation mechanism.

For a more extensive tutorial on how PyTorch internals work, please take a look on my previous tutorial on the PyTorch internal architecture.

Libtorch can be downloaded from the Pytorch website and it is only available as a preview for a while. You can also find the documentation in this site, which is mostly a Doxygen rendered documentation. I found the library pretty stable, and it makes sense because it is actually exposing the stable foundations of PyTorch, however, there are some issues with headers and some minor problems concerning the library organization that you might find while starting working with it (that will hopefully be fixed soon).

For NodeJS, I’ll use the Native Abstractions library (nan) which is the most recommended library (actually is basically a header-only library) to create NodeJS C++ add-ons and the cmake-js, because libtorch already provide the cmake files that make our building process much easier. However, the focus here will be on the C++ code and not on the building process.

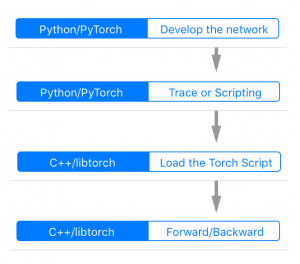

The flow for the development, tracing, serializing and loading the model can be seen in the figure on the left side.

It starts with the development process and tracing being done in PyTorch (Python domain) and then the loading and inference on the C++ domain (in our case in NodeJS add-on).

Wrapping the Tensor

In NodeJS, to create an object as a first-class citizen of the JavaScript world, you need to inherit from the ObjectWrap class, which will be responsible for wrapping a C++ component.

As you can see, most of the code for the definition of our Tensor class is just boilerplate. The key point here is that the torchjs::Tensor will wrap a torch::Tensor and we added two special public methods (setTensor and getTensor) to set and get this internal torch tensor.

I won’t show all the implementation details because most parts of it are NodeJS boilerplate code to construct the object, etc. I’ll focus on the parts that touch the libtorch API, like in the code below where we are creating a small textual representation of the tensor to show on JavaScript (toString method):

What we are doing in the code above, is just getting the internal tensor object from the wrapped object by unwrapping it. After that, we build a string representation with the tensor size (each dimension sizes) and its type (float, etc).

Wrapping Tensor-creation operations

Let’s create now a wrapper code for the torch::ones function which is responsible for creating a tensor of any defined shape filled with constant 1’s.

NAN_METHOD(ones) {

// Sanity checking of the arguments

if (info.Length() < 2)

return Nan::ThrowError(Nan::New("Wrong number of arguments").ToLocalChecked());

if (!info[0]->IsArray() || !info[1]->IsBoolean())

return Nan::ThrowError(Nan::New("Wrong argument types").ToLocalChecked());

// Retrieving parameters (require_grad and tensor shape)

const bool require_grad = info[1]->BooleanValue();

const v8::Local<v8::Array> array = info[0].As<v8::Array>();

const uint32_t length = array->Length();

// Convert from v8::Array to std::vector

std::vector<long long> dims;

for(int i=0; i<length; i++)

{

v8::Local<v8::Value> v;

int d = array->Get(i)->NumberValue();

dims.push_back(d);

}

// Call the libtorch and create a new torchjs::Tensor object

// wrapping the new torch::Tensor that was created by torch::ones

at::Tensor v = torch::ones(dims, torch::requires_grad(require_grad));

auto newinst = Tensor::NewInstance();

Tensor* obj = Nan::ObjectWrap::Unwrap<Tensor>(newinst);

obj->setTensor(v);

info.GetReturnValue().Set(newinst);

}

So, let’s go through this code. We are first checking the arguments of the function. For this function, we’re expecting a tuple (a JavaScript array) for the tensor shape and a boolean indicating if we want to compute gradients or not for this tensor node. After that, we’re converting the parameters from the V8 JavaScript types into native C++ types. Soon as we have the required parameters, we then call the torch::ones function from the libtorch, this function will create a new tensor where we use a torchjs::Tensor class that we created earlier to wrap it.

And that’s it, we just exposed one torch operation that can be used as native JavaScript operation.

Intermezzo for the PyTorch JIT

The introduced PyTorch JIT revolves around the concept of the Torch Script. A Torch Script is a restricted subset of the Python language and comes with its own compiler and transform passes (optimizations, etc).

This script can be created in two different ways: by using a tracing JIT or by providing the script itself. In the tracing mode, your computational graph nodes will be visited and operations recorded to produce the final script, while the scripting is the mode where you provide this description of your model taking into account the restrictions of the Torch Script.

Note that if you have branching decisions on your code that depends on external factors or data, tracing won’t work as you expect because it will record that particular execution of the graph, hence the alternative option to provide the script. However, in most of the cases, the tracing is what we need.

To understand the differences, let’s take a look at the Intermediate Representation (IR) from the script module generated both by tracing and by scripting.

@torch.jit.script

def happy_function_script(x):

ret = torch.rand(0)

if True == True:

ret = torch.rand(1)

else:

ret = torch.rand(2)

return ret

def happy_function_trace(x):

ret = torch.rand(0)

if True == True:

ret = torch.rand(1)

else:

ret = torch.rand(2)

return ret

traced_fn = torch.jit.trace(happy_function_trace,

(torch.tensor(0),),

check_trace=False)

In the code above, we’re providing two functions, one is using the @torch.jit.script decorator, and it is the scripting way to create a Torch Script, while the second function is being used by the tracing function torch.jit.trace. Not that I intentionally added a “True == True” decision on the functions (which will always be true).

Now, if we inspect the IR generated by these two different approaches, we’ll clearly see the difference between the tracing and scripting approaches:

As we can see, the IR is very similar to the LLVM IR, note that in the tracing approach, the trace recorded contains only one path from the code, the truth path, while in the scripting we have both branching alternatives. However, even in scripting, the always false branch can be optimized and removed with a dead code elimination transform pass.

PyTorch JIT has a lot of transformation passes that are used to do loop unrolling, dead code elimination, etc. You can find these passes here. Not that conversion to other formats such as ONNX can be implemented as a pass on top of this intermediate representation (IR), which is quite convenient.

Tracing the ResNet

Now, before implementing the Script Module in NodeJS, let’s first trace a ResNet network using PyTorch (using just Python):

As you can see from the code above, we just have to provide a tensor example (in this case a batch of a single image with 3 channels and size 224×224. After that we just save the traced network into a file called resnet18_trace.pt.

Now we’re ready to implement the Script Module in NodeJS in order to load this file that was traced.

Wrapping the Script Module

This is now the implementation of the Script Module in NodeJS:

// Class constructor

ScriptModule::ScriptModule(const std::string filename) {

// Load the traced network from the file

this->mModule = torch::jit::load(filename);

}

// JavaScript object creation

NAN_METHOD(ScriptModule::New) {

if (info.IsConstructCall()) {

// Get the filename parameter

v8::String::Utf8Value param_filename(info[0]->ToString());

const std::string filename = std::string(*param_filename);

// Create a new script module using that file name

ScriptModule *obj = new ScriptModule(filename);

obj->Wrap(info.This());

info.GetReturnValue().Set(info.This());

} else {

v8::Local<v8::Function> cons = Nan::New(constructor);

info.GetReturnValue().Set(Nan::NewInstance(cons).ToLocalChecked());

}

}

As you can see from the code above, we’re just creating a class that will call the torch::jit::load function passing a file name of the traced network. We also have the implementation of the JavaScript object, where we convert parameters to C++ types and then create a new instance of the torchjs::ScriptModule.

The wrapping of the forward pass is also quite straightforward:

As you can see, in this code, we just receive a tensor as an argument, we get the internal torch::Tensor from it and then call the forward method from the script module, we wrap the output on a new torchjs::Tensor and then return it.

And that’s it, we’re ready to use our built module in native NodeJS as in the example below:

var torchjs = require("./build/Release/torchjs");

var script_module = new torchjs.ScriptModule("resnet18_trace.pt");

var data = torchjs.ones([1, 3, 224, 224], false);

var output = script_module.forward(data);

I hope you enjoyed ! Libtorch opens the door for the tight integration of PyTorch in many different languages and frameworks, which is quite exciting and a huge step towards the direction of production deployment code.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

There are, however, other senses that we can use to monitor the training of neural networks, such as sound. Sound is one of the perspectives that is currently very poorly explored in the training of neural networks. Human hearing can be very good a distinguishing very small perturbations in characteristics such as rhythm and pitch, even when these perturbations are very short in time or subtle.

There are, however, other senses that we can use to monitor the training of neural networks, such as sound. Sound is one of the perspectives that is currently very poorly explored in the training of neural networks. Human hearing can be very good a distinguishing very small perturbations in characteristics such as rhythm and pitch, even when these perturbations are very short in time or subtle.